China��s financial opening-up has made significant achievements with its steady development. China has been forging ahead with ruled-based opening up in financial industry with higher standard, since the 14th Five-Year Plan (2021-2025) began.

A series opening-up measures has been carried out, particularly in the bond market. In 2022, foreign institutional investors are welcomed and encouraged to enter into the exchange bond market, which extends their investment scope in China. Meanwhile, the authorities have kept promoting the opening-up of the inter-bank bond market. In 2022, the People��s Bank of China (hereinafter the PBOC) issued the Provisions on the Management of Funds Invested by Foreign Institutional Investors in China's Bond Market (hereinafter as No.258 [2022] of the PBOC and the SAFE, Circular 258), jointly with the State Administration of Foreign Exchange (hereinafter the SAFE), unifying the rules on fund management in the bond market. It clarifies that foreign institutional investors may remit in any currency to invest in the PRC bond market. Further, the PBOC Work Conference in 2023 highlights the principle of continuously optimizing the international financial cooperation and opening up.

The favorable policies attract the attention of some overseas investors and recently, we received more relevant inquiries from overseas investment institutions. There are no doubts that overseas investors are highly interested in China's capital markets. However, they still have concerns about the enforceability of the supporting policies and measures.

Given that, we are trying to introduce the ongoing financial opening-up policy in detail in articles in this series, by systematically elaborating and analyzing the approaches and schemes for overseas investors�� entering PRC bond market, stock market and foreign exchange market.

We introduce the application procdure and trading rules in our previous article: Access to PRC Capital Martkets-CIBM Direct(I). Next, we would like to focus on account management and taxation in relation to CIBM Direct.

3. Management of Capital Accounts

Since there is no policy on the management of capital account specifically applicable to CIBM Direct, the general regulation for CIBM (Circular 258) is applied. In accordance with Circular 258, the settlement agent shall be entrusted to conduct issues related to capital account management. Besides, any currency may be used to be invested in the CIBM, while RMB Cross-border Interbank Payment System (CIPS) are encouraged.

3.1 Registration of CIBM Funds

Funds of foreign investors in CIBM shall be filed and registered as the SAFE required.

The custodian or settlement agent shall conduct filing and registration on behalf of the foreign institutional investor via the SAFE��s Capital Account Information System. The filing and registration shall be completed within 10 business day upon obtaining the Filing Notice of Market Access to the Chinese Inter-bank Bond Market or any other equivalent document(s).

3.2 Opening Up and Account Management

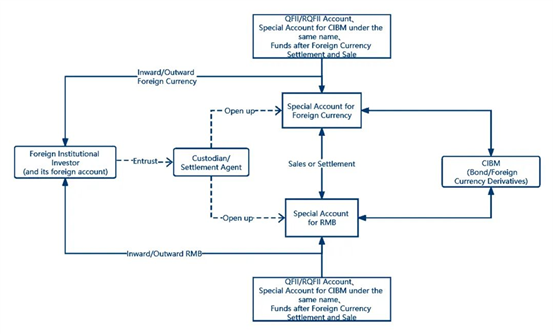

Foreign institutional investors shall open up a special capital account for their investments in PRC bond market as required, including a RMB account and a foreign currency account. The special capital accounts shall be exclusively used in CIBM and foreign exchange derivatives transactions within hedging need.

3.2.1 Method of Fund Flow

A special foreign currency account and a special RMB account shall be opened by the custodian or settlement agent. The two accounts are used for the separate management of the foreign currency and RMB funds remitted in or out of CIBM.

The following principles shall be complied with:

- Used for investment in the Chinese bond market only;

- Cross-currency regulatory arbitrage is abandoned;

- Foreign exchange derivatives can be invested only for the need of hedging and management of foreign exchange risk exposure arising from the investments in CIBM.

Mode of fund flow shows as the following picture:

3.2.2 Range of Receipt and Payment of Special Foreign Currency/RMB Accounts

Catering for the mode of fund flow and relevant principles mentioned above, the receipt and payment range of the special accounts have been stated in Circular 258.

Range of Receipt:

- Principal and related taxes (taxes, custodian fees, audit fees, management fees, etc.) remitted by foreign institutional investors from overseas,

- Proceeds from bond sales, principal recovered upon maturity of bonds

- Interest income

- Inward remittance related to bond and foreign exchange derivatives transactions

- Inward remittance related to foreign exchange settlements and sales in the PRC jurisdiction

- Transfers of funds among the special accounts under the same name

- Inward remittance of funds from the special domestic account of QFII/ RQFII under the same name

- Other income in compliance with the regulations of the PBOC and the SAFE.

Range of Payment:

- Payment of bond transaction price and related taxes

- Outward remittance of investment principal and proceeds

- Outward remittance related to bond and foreign exchange derivatives transactions

- Outward remittance of funds related to foreign exchange purchases and sales in the PRC jurisdiction

- Transfers among the special accounts under the same name

- Outward remittance from the special domestic account of QFII/RQFII under the same name

- Other payment in compliance with the regulations of the PBOC and the SAFE.

3.2.3 Regulation of Inward or Outward Remittance

3.2.3.1 Currency Ratio between Inward and Outward

To prevent cross-currency regulatory arbitrage, the authorities regularly impose restrictions on inward and outward remittances of foreign currency.

Under the invalid Notice of the State Administration of Foreign Exchange on the Issues of Foreign Exchange Administration concerning Foreign Institutional Investors' Investment in the Interbank Bond Market (No.12 [2016] of the SAFE, hereinafter Circular 12), the maximum fluctuation of any kind of currency between the inward remittance and outward remittance shall be 10%. The ratio is permitted to be higher if the fund of foreign institutional investors remits outward PRC for the first time.

Circular 258 again relaxes such restriction in 2023.that the cumulative amount of any currency to be remitted outward PRC shall not exceed 120% of that remitted inward. Furthermore, a looser policy could be applied if the investor intends to invest in CIBM for long term. With no doubt, it reflects the SAFE��s determination of the wider opening up of the Chinese financial market.

3.2.3.2 Compliance

The SAFE requires that the custodians and settlement agents shall review the authenticity and compliance of fund flow, and regularly submit trading information and statistics to the authorities, so as to prevent money laundering and terrorist financing.

3.3 Regulations on Foreign Exchange Derivatives Investments

Foreign investors can not only invest in cash bonds through CIBM Direct, but also conduct derivatives transactions based on their hedging need.

Investors may choose various trading mechanisms such as rollover, reverse position closing, gross or balance settlement, and settle their gains or losses in RMB or foreign currencies.

To prevent regulatory arbitrage, the SAFE has additional regulations on derivatives transaction.

3.3.1 Registration and Filing

Pursuant to Circular 258, investment in foreign exchange derivatives shall be additionally filed and registered with the China Foreign Exchange Trading Center, which can be conducted on their own or through their custodians or settlement agents.

3.3.2 Written Commitment Letter of Hedging

To prevent regulatory arbitrage, the SAFE requires investors to issue a written commitment to promise that the derivatives transaction is only for hedging need.

3.3.3 Transaction Restrictions

The SAFE requires that the exposure of foreign exchange derivatives shall be reasonably related to the exposure of foreign exchange risks.

The SAFE requires also that the investor shall adjust the change of foreign exchange risk exposure due to bond investments within five business days or within the first five business days of the next month.

4. Taxation on CIBM Direct

The tax policies of foreign investors investing in the traditional interbank bond market shall be applied to CIBM Direct.

4.1 Taxation on Bond Interest Income

According to the Announcement of the Ministry of Finance and the State Taxation Administration on Continuing the Enterprise Income Tax and Value-Added Tax Policies for Overseas Institutions' Investment in the Domestic Bond Market (No.34 [2021] of the Ministry of Finance and the State Administration of Taxation, hereinafter as Circular 34), the bond interest income of overseas institutions derived from investments in the PRC bond market is temporarily exempt from corporate income tax and value-added tax. Therefore, the bond interest income obtained by foreign institutional investors from CIBM Direct is not subject to corporate income tax and value-added tax.

4.2 Taxation on Transferring Bonds

Currently, there are no special regulations on the foreign institutional investor taxation of transferring bonds. Thus, Enterprise Income Tax Law of the People's Republic of China (2018 Amendment) are applied.

A foreign institutional investor is a non-resident enterprise that have no branch or establishment in China but have income sourced from China. Its income derived from transferring bond, deemed as one kind of income from asset transferring, shall be taxed 20%.

5. Conclusion

Compared with the traditional CIBM mode via a settlement agent to trade, CIBM Direct simplifies the quotation process. But rules of CIBM Direct are consistent with the general principles.

By the beginning of 2022, CIBM Direct had attracted 431 foreign commercial institutional investors and 76 sovereign investors around the world, making it one of the major accesses available for foreign institutional investors to invest in the PRC bond market. It indicates overseas investors�� relatively positive attitude towards the innovative tools.

The remaining concerns of foreign investors towards the CIBM Direct lie mainly in the overall environment for PRC financial markets, such as unfamiliar procedures, illiquidity and insufficient hedging tools. In this regards, Chance Bridge will continuously follow up the relevant policies and regularly update our study.

Link��Access to PRC Capital Martkets:CIBM Direct(I)

The Financial Markets Team of Chance Bridge

Based on its extensive project experience and excellent market performance, the Financial Markets team of Chance Bridge has won awards and commendations as "Law Firm of the Year �C Structured Finance/Asset Securitization�� by China Business Law Journal and "Notable Law Firms in 2021 (Banking & Finance, M&A)�� and "Recommended Law Firm (Bonds, Structured Finance and Asset Securitization)" by IFR1000 and other leading rating agencies.

The Financial Markets Team of Chance Bridge focuses its work in the areas of asset management plans, trust plans, securitization projects, private equity funds, financial derivatives and other related areas. Our broad practical experience and research achievements are trusted and recognized by our clients. We combine non-litigation and litigation capabilities in order to provide comprehensive and holistic legal solutions to our clients based on a full understanding of financial trading practices, financial laws and regulations.

As an early PRC law firm involved in structured financial product transactions such as asset securitization, the Financial Markets Team of Chance Bridge specializes in transaction structuring, transaction terms design and compliance analysis of new financial products, and providing tailored legal programs for different products. The members of the team also focus on the resolution of complex and difficult disputes in respect of innovative financial products, and have extensive experience and have achieved successful results for our clients a wide range of structured finance transactions. We devote substantial attention to controlling regulatory compliance requirements and transaction security issues from a financial dispute resolution perspective, and thus are able to provide forward-looking suggestions on solutions for financial institutions' business promotion.

- Compliance Issues Arising from Going Abroad and Operating Overseas ---How to work well on antitrust compliance

- Merger Control Filing Related to Private Equity Funds

- Draft for Soliciting Opinions on the Anti-Monopoly Guidelines in the Pharmaceutical Sector Released: Key Highlights for Pharmaceutical Companies